Several government-backed savings schemes in India are currently offering annual interest rates of 7.5 percent and above, based on the latest notified rates. These instruments form part of the Centre’s small savings framework, with rates reviewed periodically.

The schemes differ in tenure, eligibility, and payout structures. Some are targeted at specific groups such as senior citizens or girl children, while others are open to all investors. Their relatively stable returns and tax benefits make them attractive to conservative investors.

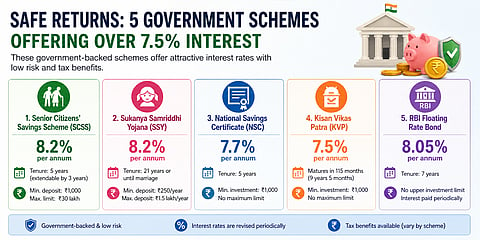

Here are five options offering 7.5 percent or more:

The scheme offers 8.2 percent per annum. The minimum deposit is ₹1,000, with a maximum cap of ₹30 lakh across all accounts held by an individual.

Tenure: 5 years, extendable by 3 years

Premature withdrawal allowed under conditions

Eligibility:

Individuals aged 60 years and above

Individuals aged 55–60 years under VRS or superannuation

Retired defence personnel aged 50 years and above (with conditions)

This scheme for a girl child also offers 8.2 percent per annum and provides tax-free maturity benefits. Under the old tax regime, deposits up to ₹1.5 lakh annually qualify for deductions.

Minimum deposit: ₹250 per year

Maximum deposit: ₹1.5 lakh per year

Tenure: 21 years or until marriage

Contributions are required for 15 years, with the balance continuing to earn interest thereafter.

NSC offers 7.7 percent per annum, compounded annually, with returns paid at maturity.

Tenure: 5 years

Minimum investment: ₹1,000

No maximum limit

Accounts can be opened by individuals or on behalf of minors. The scheme also allows loans against the certificate.

KVP offers 7.5 percent per annum and doubles the investment in 115 months (9 years and 5 months).

Minimum investment: ₹1,000

No maximum limit

PAN is mandatory for investments above ₹50,000, while income proof is required for deposits above ₹10 lakh.

The Reserve Bank of India’s floating rate bond currently offers 8.05 percent per annum.

Tenure: 7 years

No upper investment limit

Interest paid periodically

The bonds carry a sovereign guarantee and are considered among the safest fixed-income options. They often offer higher returns compared to many bank fixed deposits.

Interest rates are revised periodically by the government

Tax treatment varies across schemes

Liquidity differs, with some schemes locking in funds for longer periods

For investors seeking stability over high returns, these schemes continue to be reliable options in the current rate environment.

(By arrangement with livemint.com)