With the deadline for filing income-tax returns (ITR) for the financial year 2025-26 (assessment year 2026-27) extended to August 31, first-time taxpayers have more time to complete the process. However, waiting until the last minute could lead to technical glitches, errors and delayed refunds. A little preparation can make filing your first return quick and hassle-free.

The Income Tax Department has already enabled the Excel utilities for ITR-1, ITR-2, ITR-3, ITR-4, ITR-5 and ITR-7, allowing taxpayers to prepare returns offline before uploading them through the e-filing portal.

Avoid heavy traffic on the e-filing portal near the deadline

Get tax refunds processed faster

Have enough time to correct mistakes or respond to notices

Reduce the risk of missing mandatory documents

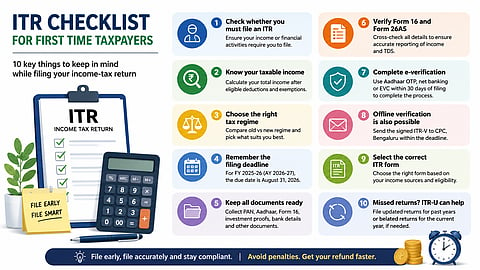

Filing an income-tax return is mandatory if your income exceeds the prescribed exemption limit. You may also need to file a return if you meet certain specified financial criteria, including:

Holding assets in India or abroad

Investing in shares, securities or ESOPs

Bank deposits exceeding ₹50 lakh

Savings or current account transactions exceeding ₹1 crore

Annual electricity bills above ₹1 lakh

Overseas travel expenditure above ₹2 lakh

Business sales exceeding ₹60 lakh

Your taxable income is calculated after deducting eligible exemptions and deductions from your total income.

Besides salary, taxable income may include:

Interest from bank deposits

Capital gains

Dividend income

Rental income

Other taxable earnings

Eligible deductions may include investments in:

Public Provident Fund (PPF)

National Pension System (NPS)

Life insurance

Home loan interest

Other tax-saving investments

Taxpayers can opt for either the old tax regime or the new tax regime.

The better option depends on:

Your salary level

Eligible deductions and exemptions

Tax-saving investments

Using an online tax calculator or consulting a chartered accountant can help identify the more tax-efficient option.

For FY 2025-26 (AY 2026-27):

Due date for filing without penalty: August 31, 2026

Belated returns can be filed up to December 31, 2026

Late filing may attract a penalty depending on the delay and tax payable

Before starting the filing process, keep these documents handy:

PAN card

Aadhaar card (linked with PAN)

Form 16 from your employer

Bank account details

Investment proof

Home loan interest certificate, if applicable

Insurance premium receipts

Details of other income

Do not rely only on Form 16.

Cross-check the following:

Form 16 issued by your employer

Form 26AS

Annual Information Statement (AIS)

These documents help verify:

Tax deducted at source (TDS)

Interest income

Dividend income

Securities transactions

Foreign remittances

Other reported financial transactions

Matching these records reduces the chances of receiving tax notices later.

Filing is not complete until the return is verified.

You can e-verify using:

Aadhaar OTP

Net banking

Electronic Verification Code (EVC)

Failure to complete verification within 30 days could delay processing of the return and any refund due.

Those unable to complete e-verification can verify their return by sending the signed ITR-V acknowledgement to the Centralised Processing Centre (CPC) in Bengaluru within the prescribed time limit.

Choosing the wrong form may result in rejection of the return.

The commonly used forms include:

ITR-1 (Sahaj): Salaried individuals with one house property and income from other sources

ITR-2: Individuals and Hindu Undivided Families (HUFs) without business income

ITR-3: Individuals or HUFs having business or professional income

ITR-4 (Sugam): Taxpayers opting for the presumptive taxation scheme

The Income Tax e-filing portal also offers a "Help me decide" feature to guide users to the appropriate form.

Taxpayers who failed to file returns for any of the previous assessment years can use the updated return facility (ITR-U), subject to applicable conditions.

For the current assessment year, taxpayers who miss the August 31 deadline can still submit a belated return, although they may have to pay a late filing fee and interest on any outstanding tax liability.

For first-time taxpayers, the income-tax filing process can appear complicated, but proper preparation makes it much easier. Keeping the necessary documents ready, selecting the correct form, reconciling tax details with Form 26AS and AIS, and completing verification on time can help avoid penalties, delays and unnecessary compliance issues. Filing well before the deadline also leaves enough room to correct mistakes, if any.