Seema thought the jewellery and cash gifts she received from a family friend were entirely tax-free—until a tax notice arrived. Since the total value exceeded ₹50,000 and was not disclosed, the entire amount became taxable in her hands. Many taxpayers make similar mistakes due to a lack of clarity on how gift taxation works under Indian law.

Any gift received—whether in cash, movable assets or immovable property—becomes taxable if the aggregate value exceeds ₹50,000 in a financial year. Once this threshold is breached, the entire amount (not just the excess) is taxed as income in the hands of the recipient.

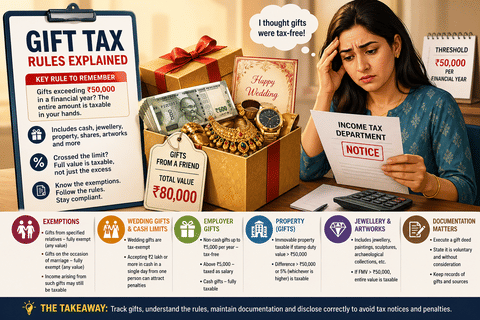

Gifts include cash, jewellery, shares, property and artworks

Threshold: ₹50,000 per financial year (aggregate value)

If crossed, the full amount becomes taxable

Example: If total gifts received are ₹80,000, the entire ₹80,000 is taxable. If the value remains within ₹50,000, no tax applies.

Certain categories of gifts are fully exempt, regardless of value.

Gifts from specified relatives (spouse, parents, siblings, in-laws)

Gifts received on the occasion of marriage (from any person)

Key caveat:

Income generated from such gifts (interest, rent, etc.) may still be taxable under clubbing provisions

Aggregation rule often missed:

Multiple gifts from friends exceeding ₹50,000 in total will make the entire amount taxable

While wedding gifts enjoy full tax exemption, cash transactions face separate restrictions.

Gifts received at the time of marriage are fully tax-free

However, accepting ₹2 lakh or more in cash in a single day from one person can attract penalties

It is advisable to receive such gifts within a reasonable period around the wedding

Non-cash gifts (vouchers, tokens) are tax-free up to ₹5,000 per year

Any amount beyond ₹5,000 is treated as salary and taxed as per slab

Cash gifts from employers are fully taxable without any exemption

Immovable property received without consideration is taxable if stamp duty value exceeds ₹50,000

If property is purchased below stamp duty value by more than ₹50,000 or 5 percent (whichever is higher), the difference is taxed

Movable assets: jewellery and artworks

Includes jewellery, paintings, sculptures, archaeological collections and other works of art

If received as a gift and fair market value exceeds ₹50,000, the entire value is taxable

Documentation matters

A gift deed should be executed for high-value gifts

The document must state that the transfer is voluntary and without consideration

Maintaining records helps respond to tax notices and ensures compliance

Gift taxation rules in India are clear but often misunderstood. The ₹50,000 threshold, exemptions for relatives and weddings, and specific provisions for property and employer gifts make it essential for taxpayers to track, document and disclose such receipts carefully.

(By arrangement with livemint.com)